A strong F&I Manager can have a major impact on dealership profitability. The right person can improve product penetration, protect the reserve, increase deal flow, reduce funding delays, and improve the customer experience after the vehicle sale.

However, the pay plan matters.

If the plan rewards only gross, you may achieve short-term production gains but create long-term problems with chargebacks, compliance risks, customer complaints, or uneven product presentation. If the plan is too soft, you may not properly reward high performers who drive real finance department results.

At CarGuys Inc., we work with dealerships across North America that are trying to recruit, evaluate, and retain strong automotive talent. One pattern is clear: the best F&I pay plans balance production with quality. They reward profit, but they also protect the store.

Why F&I Pay Plans Need More Balance

F&I is one of the most important profit centers in a dealership, but it is also one of the most sensitive.

A good pay plan should motivate the F&I Manager to increase revenue while still supporting:

- Consistent product presentation

- Strong product penetration

- Clean paperwork

- Fast funding

- Low chargebacks

- Compliance with dealership and lender standards

- A positive customer experience

When a pay plan focuses too heavily on one area, behavior can drift.

For example, a plan based almost entirely on backend gross may encourage aggressive selling but ignore chargeback exposure. A plan that relies heavily on reserves may create lender mix issues. A plan with no compliance component may expose the dealership to avoidable risk.

The goal is not to make the plan complicated. The goal is to make it clear, fair, and aligned with how the dealership actually wants F&I to operate.

Key Areas to Include in an F&I Manager Pay Plan

1. Backend Gross Profit

Backend gross is still the foundation of most F&I compensation plans. The F&I Manager should be rewarded for producing finance income, service contracts, GAP, maintenance plans, appearance protection, tire and wheel, and other approved products.

However, gross alone should not be the only measurement.

A pay plan that rewards only gross can create pressure to maximize every deal, regardless of long-term customer satisfaction or chargeback risk.

2. Product Penetration

Product penetration helps measure whether the F&I Manager is consistently presenting the dealership’s value-added products.

Common product penetration categories include:

- Vehicle service contracts

- GAP

- Maintenance plans

- Tire and wheel

- Appearance protection

- Key replacement

- Ancillary protection products

Penetration bonuses can be especially useful because they reward consistency rather than just big individual deals.

3. Finance Reserve

Reserve is still important, but many dealerships are more cautious about how much weight they give it. Lender relationships, rate environment, compliance expectations, and customer trust all matter.

A smart plan can reward reserve performance without encouraging behavior that could lead to future complaints or funding issues.

4. Chargebacks

Chargebacks can quietly eat away at the profit that looked great on paper.

If an F&I Manager is paid heavily upfront with no chargeback accountability, the dealership may end up rewarding production that does not stick.

A good plan should include either:

- A chargeback reserve

- A chargeback adjustment

- A bonus threshold tied to acceptable chargeback levels

This does not mean punishing the manager for every cancellation. Some chargebacks are unavoidable. However, the plan should encourage clean selling, realistic product recommendations, and customer retention.

5. Compliance and Funding Quality

Compliance should not be treated as an afterthought.

F&I Managers handle sensitive areas including credit applications, disclosures, lender requirements, product menus, signatures, and deal documentation. Mistakes can create legal, financial, and reputational problems for the store.

A practical plan can include a compliance bonus, or it can make compliance a condition for receiving other bonuses.

Funding quality also matters. Delayed funding slows cash flow and creates friction between sales, accounting, and F&I.

Example of a Practical F&I Manager Pay Plan

Below is a sample structure a dealership could use as a starting point. The exact numbers should be adjusted based on store volume, average backend gross, market, lender mix, product lineup, and overall compensation targets.

Sample Monthly F&I Pay Plan

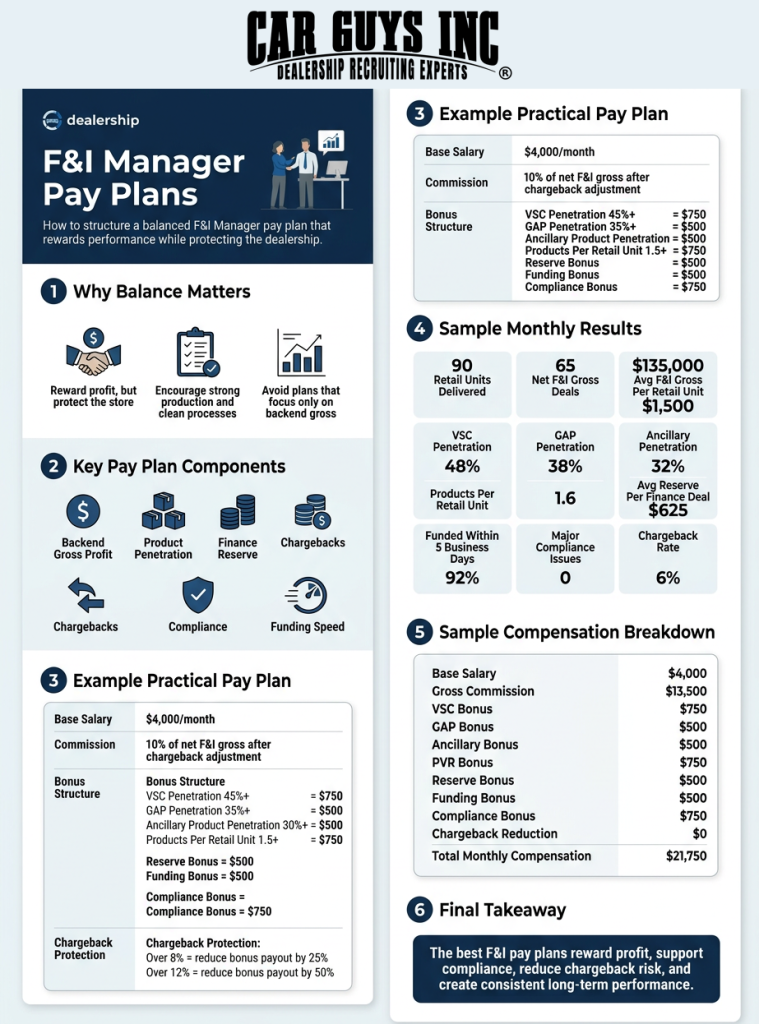

Base Salary:

$4,000 per month

Commission on Net F&I Gross:

10% of net F&I gross after chargeback adjustment

Product Penetration Bonus:

Paid monthly if minimum volume is met.

| Metric | Target | Bonus |

| Vehicle Service Contract Penetration | 45% or higher | $750 |

| GAP Penetration | 35% or higher on finance deals | $500 |

| Maintenance or Ancillary Product Penetration | 30% or higher | $500 |

| Total Product Per Retail Unit | 1.5 products or higher | $750 |

Reserve Bonus:

$500 monthly bonus if the finance reserve averages at least $600 per financed deal while maintaining lender and compliance standards.

Funding Bonus:

$500 monthly bonus if 90% or more of funded deals are approved and funded within 5 business days.

Compliance Bonus:

$750 monthly bonus if there are no major compliance violations, missing required disclosures, or preventable documentation issues.

Chargeback Protection:

If monthly chargebacks exceed 8% of the prior 90-day F&I gross, reduce the monthly bonus payout by 25%. If chargebacks exceed 12%, reduce the monthly bonus payout by 50%.

Sample Pay Plan Calculation

Here is how the plan could work in a real month.

Monthly Department Results

| Category | Result |

| Retail Units Delivered | 90 |

| Finance Deals | 65 |

| Net F&I Gross | $135,00 0 |

| Average F&I Gross Per Retail Unit | $1,500 |

| Vehicle Service Contract Penetration | 48% |

| GAP Penetration | 38% |

| Ancillary Product Penetration | 32% |

| Products Per Retail Unit | 1.6 |

| Average Reserve Per Finance Deal | $625 |

| Deals Funded Within 5 Business Days | 92% |

| Major Compliance Issues | 0 |

| Chargeback Rate | 6% |

Monthly Compensation Example

| Pay Component | Amount |

| Base Salary | $4,000 |

| 10% Commission on $135,000 Net F&I Gross | $13,500 |

| VSC Penetration Bonus | $750 |

| GAP Penetration Bonus | $500 |

| Ancillary Product Bonus | $500 |

| Products Per Retail Unit Bonus | $750 |

| Reserve Bonus | $500 |

| Funding Bonus | $500 |

| Compliance Bonus | $750 |

| Chargeback Reduction | $0 |

| Total Monthly Compensation | $21,750 |

In this example, the F&I Manager is well compensated because the department performed well across multiple areas. The plan rewards gross, but it also rewards product consistency, fast funding, compliance, and low chargebacks.

That balance is the point.

Why This Type of Plan Works

This structure gives the F&I Manager clear financial upside while keeping the dealership protected.

It rewards the behaviors most stores actually want:

- Strong backend production

- Consistent product presentation

- Healthy reserve performance

- Clean paperwork

- Fast funding

- Low chargebacks

- Compliance discipline

It also helps reduce internal conflict. Sales managers, general managers, accounting teams, and owners all benefit when F&I is not just producing gross, but producing clean, fundable, sustainable gross.

What to Avoid in an F&I Pay Plan

Dealerships should be careful with pay plans that are too one-dimensional.

Common mistakes include:

- Paying only on gross with no chargeback accountability

- Ignoring product penetration

- Over-rewarding reserve without compliance guardrails

- Creating too many confusing bonus tiers

- Changing the plan too often

- Setting unrealistic targets that employees do not believe are attainable

- Failing to explain how chargebacks are calculated

- Not tying any part of the plan to funding or paperwork quality

An F&I Manager should understand exactly how they are paid, what results matter most, and how performance is measured.

Confusion kills motivation.

Pay Plan Design Also Affects Recruiting

Strong F&I Managers usually know their value. When they evaluate a new opportunity, they are not only looking at the top-line earning potential.

They also want to know:

- Is the pay plan realistic?

- Is the store volume strong enough to support the income?

- Are the products competitive?

- Does the dealership have good lender relationships?

- Are chargebacks handled fairly?

- Is the sales process organized?

- Does management support F&I?

- Are compliance expectations clear?

If a dealership wants to attract serious F&I talent, the compensation structure needs to feel professional, transparent, and achievable.

This is where many stores lose candidates. They advertise a high-earning range, but the actual pay plan is vague, confusing, or built on unrealistic assumptions.

Wrapping It Up

A good F&I Manager pay plan should do more than reward gross profit. It should guide behavior.

The best plans create a balance between production and protection. They give the F&I Manager meaningful upside while also supporting compliance, customer satisfaction, funding speed, and long-term profitability.

For dealerships, that balance can make a real difference. The right pay plan can help attract better candidates, retain stronger performers, and create a more consistent F&I process across the store.

At CarGuys Inc., we understand that hiring the right F&I Manager is not just about filling a seat. It is about finding someone who can produce, lead the process, protect the dealership, and support the customer experience from delivery through funding.

CarGuys Inc. is an automotive sales & finance management recruiting company built exclusively for the car business. From technicians and service advisors to salespeople and managers, we connect dealerships and repair shops with qualified talent faster, using nationwide reach and years of hands-on experience.

With over 700 clients and thousands of hires, we don’t just fill positions.

We help build stronger teams that foster long-term success.